The radioligand therapy (RLT) sector is experiencing a period of explosive growth, transitioning from a niche area of oncology into a strategic battleground for major pharmaceutical companies. This transformation is driven by the blockbuster commercial success of therapies like Pluvicto® and Lutathera®, fueling a surge in investment, multi-billion-dollar M&A activity, and a robust pipeline of over 320 clinical trials. The dominant technological trend is a strategic pivot toward more potent alpha-emitting isotopes like Actinium-225 (²²⁵Ac) and Lead-212 (²¹²Pb).

However, this rapid expansion is colliding with a fragile and underdeveloped clinical infrastructure, creating the industry's central paradox. The primary constraints on RLT development are not scientific potential but severe, interconnected bottlenecks, including a critical shortage of trial-ready clinical sites, a scarcity of specialized talent (nuclear physicians, physicists, radiopharmacists), and fragile isotope supply chains. These operational hurdles create significant delays and increase the complexity of trial execution.

In response, new business models are emerging to address this infrastructure gap. These include the development of specialized, purpose-built clinical research sites like Ohio River Valley Theragnostics (ORT), which offer an integrated, non-competitive model to accelerate trials for sponsors. In underserved regions like Latin America, companies like Synapse Global Theragnostics are implementing turnkey solutions to transform existing hospitals into self-sufficient, world-class theranostics centers. This has also spurred the growth of a dedicated ecosystem of specialist service partners—including CROs, imaging labs, and dosimetry providers—that sponsors are leveraging to navigate the unique challenges of RLT development.

1. Market Dynamics: Unprecedented Growth and Investment

The RLT market is undergoing a period of intense growth, validated by major clinical and commercial successes that have attracted massive capital investment and reshaped the competitive landscape.

Market Projections and Scale

Multiple sources confirm a significant upward trajectory for the radiopharmaceutical and theranostics markets:

Global Radiopharmaceuticals: Projected to grow from $6.8 billion in 2024 to over $14 billion by 2032. Another projection sees growth from $6.8 billion in 2024 to $12.2 billion by 2030, a 10.3% CAGR.

Global Theranostics: Projected to grow from $3.7 billion in 2023 to $12.7 billion by 2029, a 24% CAGR.

Latin America Theranostics: An untapped market projected to grow from $1.35 billion in 2025 to $3.44 billion by 2033, a 12.44% CAGR.

Nuclear Medicine: A broader category projected to grow from $13.2 billion in 2025 to $35.0 billion by 2034, an 11.4% CAGR.

The "Pluvicto Effect": Validation and Consolidation

The clinical and commercial success of Novartis's Pluvicto® has served as a primary catalyst for the industry's expansion.

Commercial Success: Pluvicto achieved $1 billion in its first year of sales and is predicted to reach $3.5 billion by 2028. Lutathera® is predicted to reach $788 million by 2028.

M&A Activity: This success has triggered a wave of multi-billion-dollar acquisitions as major pharmaceutical companies move to secure RLT platforms, talent, and manufacturing capabilities.

Bristol Myers Squibb acquired RayzeBio for $4.1 billion.

AstraZeneca acquired Fusion Pharmaceuticals for $2.4 billion.

Novartis acquired Endocyte for $2.1 billion and Mariana Oncology for $1.75 billion.

Eli Lilly acquired POINT Biopharma for $1.4 billion.

In total, Bristol Myers, AstraZeneca, and Lilly have committed $7.9 billion to acquire targeted radiotherapy assets.

The Competitive Pipeline

The influx of investment has generated intense competition and a crowded clinical pipeline.

Companies: 68 companies are currently developing RLTs, with 43 at the clinical stage.

Active Trials: There are 121 current clinical trials, with a global landscape of over 320 active trials noted. The breakdown is as follows:

Phase 1: 38 trials

Phase 1/2: 30 trials

Phase 2: 41 trials

Phase 2/3: 1 trial

Phase 3: 11 trials

2. The Infrastructure Paradox: Core Bottlenecks Stifling Growth

The explosive growth in RLT development is severely constrained by a fragile, underdeveloped clinical infrastructure. These interconnected bottlenecks are the primary rate-limiting factor for the industry.

The Triad of Scarcity

A systemic shortage of physical, human, and material resources creates a drag on the entire development ecosystem.

Clinical Site Deficit: There is a critical shortage of clinical sites equipped and licensed to support RLT trials.

Most existing trial sites lack the required combination of in-house PET/CT, SPECT, radiopharmacy, and clinical expertise.

This forces sponsors to juggle multiple vendors, slowing timelines and increasing costs.

The problem is acute in regions like Latin America, which has only 0.47 PET scanners per million people compared to the recommended 2.0-2.5, leading to underutilization of existing equipment due to supply chain failures.

The Human Capital Crisis: There is a severe shortage of the essential multidisciplinary team required for RLT trials.

The demand for VPs of Clinical Development and CMOs with direct alpha-emitter experience is estimated to exceed the available talent pool by a factor of 5 to 1.

This scarcity drives compensation packages to a 20-25% premium over equivalent roles in traditional oncology.

The ideal RLT leader is a rare "tri-brid" professional with deep expertise in clinical oncology, nuclear medicine/physics, and seasoned pharmaceutical development.

Isotope Supply Chain Fragility: The strategic pivot to alpha-emitters exacerbates an already critical bottleneck in isotope supply.

Control over the manufacturing and isotope supply chain has become a paramount strategic advantage.

In Latin America, 85% of radiopharmaceuticals must be imported, leading to frequent disruptions.

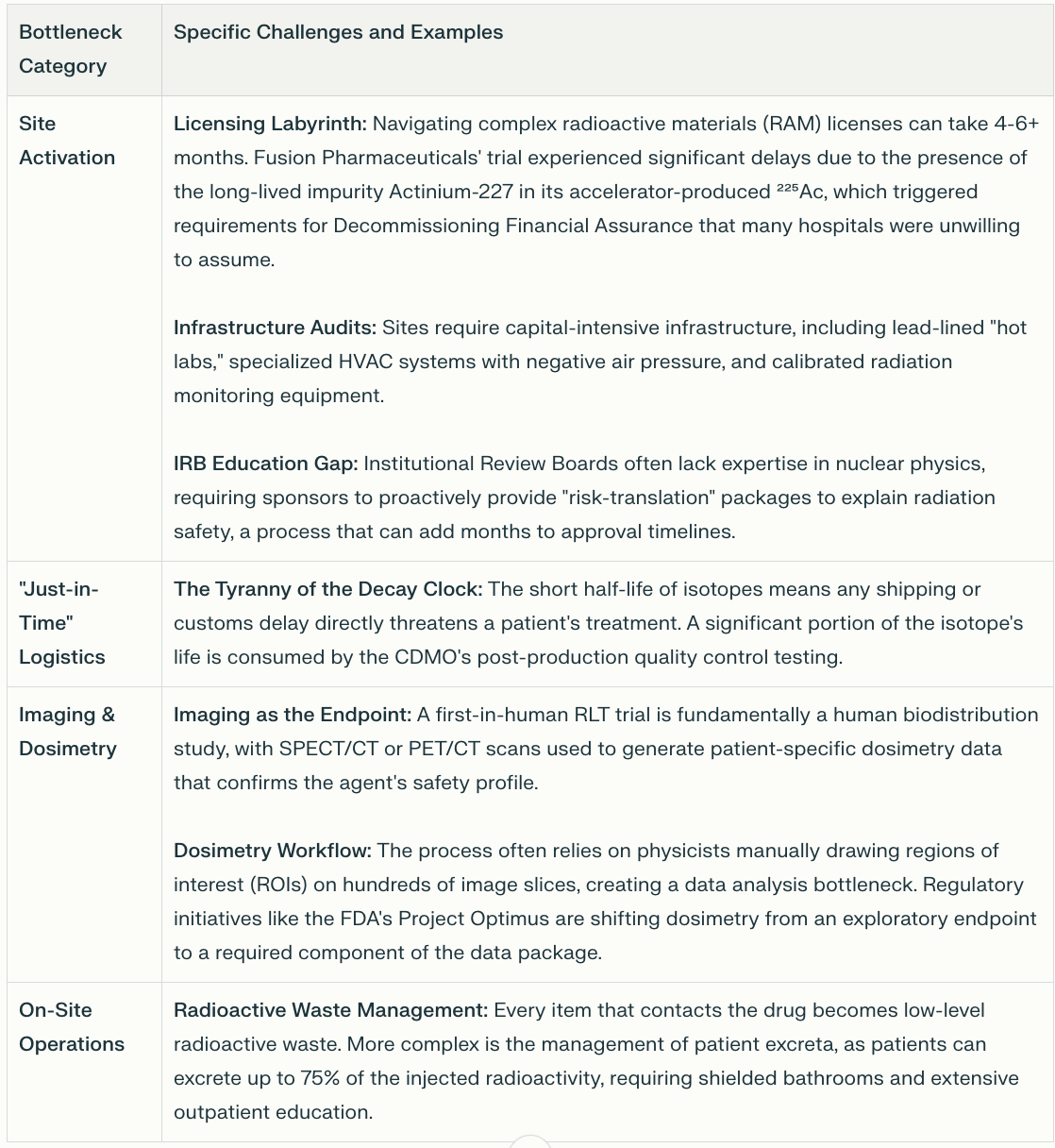

The RLT Trial Execution Gauntlet

RLT trials present unique operational hurdles that do not exist in traditional oncology, requiring deep specialist expertise.

The RLT Trial Execution Gauntlet

3. Evolving Strategies and the Competitive Landscape

The RLT battlefield is defined by a technological race toward more potent isotopes and highly differentiated corporate strategies to secure a competitive edge.

The Alpha Emitter Revolution

The dominant technological trend is the strategic pivot from beta-emitters (like ¹⁷⁷Lu) to alpha-emitting isotopes (like ²²⁵Ac and ²¹²Pb), which promise greater potency and the ability to overcome treatment resistance. Over 70% of new trial starts in the last 18 months have involved alpha-emitters or novel targets. The next frontier of isotopes includes:

Terbium-161 (¹⁶¹Tb): A beta-emitter that also releases Auger electrons, potentially enhancing potency.

Terbium-149 (¹⁴⁹Tb): A "theranostic" isotope that is both an alpha-emitter (therapy) and a positron-emitter (PET imaging).

Radium-224 (²²⁴Ra): The parent isotope for a novel intratumoral approach that releases alpha-emitting daughters directly within the tumor.

Comparative Strategic Analysis of Key RLT Developers

Comparative Strategic Analysis of Key RLT Developers

Key Regulatory Lessons

Recent clinical trial outcomes have provided critical cautionary tales for the industry, setting a higher bar for new market entrants.

The Importance of Overall Survival (OS): The pivotal trials for POINT/Lilly's PNT2002 (SPLASH) and Actinium's Iomab-B (SIERRA) were ultimately unsuccessful from a regulatory or commercial standpoint despite meeting their primary endpoints (rPFS and dCR, respectively). In both cases, a weak or confounded OS signal was the critical issue, demonstrating the supreme importance of this endpoint for regulators, particularly in competitive indications.

The Theranostic Pair Challenge: The path to securing reimbursement for a companion diagnostic PET agent can be a decade-long challenge, as illustrated by the history of amyloid PET tracers for Alzheimer's disease. Effective January 1, 2025, CMS will provide separate payment for diagnostic radiopharmaceuticals with a per-day cost exceeding a $630 threshold, a policy that will profoundly influence future pricing and market access strategies.

4. Emerging Models and Solutions

In response to the industry's infrastructure crisis, several new business and clinical delivery models are emerging to expand access, accelerate timelines, and de-risk development.

The Purpose-Built Clinical Site Model: Ohio River Valley Theragnostics (ORT)

ORT represents a model of a specialized, full-spectrum clinical research site built exclusively for RLT trials (Phase 0-3).

Mission: To provide pharmaceutical sponsors a comprehensive, streamlined, and cost-effective site to expedite RLT drug development.

Location: Strategically located in the Greater Cincinnati area, targeting an addressable regional market of an estimated 28,000 new annual cancer cases.

Integrated Capabilities: Combines PET/CT and SPECT imaging, an in-house radiopharmacy, and therapy administration under one roof.

Expert Team: Led by experienced M.D. and PhD drug developers, including a lead developer of Pluvicto.

Business Model: Operates as a non-competitive, referral-based partner for community oncologists, designed to complement, not replace, existing practices.

Financials: The company is raising $15 million. Key assumptions include enrolling 25 patients across 5 studies in Year 1, reaching 154 patients by Year 5, with a breakeven point of 67 patients per year. The first patient is targeted for Q3 2026.

The Turnkey Infrastructure Model: Synapse Global Theragnostics

Synapse delivers a proven, turnkey Management Services Organization (MSO) model to transform hospitals in Latin America into world-class theranostics centers.

Mission: To solve the "infrastructure paradox" in Latin America, where hospitals with multi-million-dollar PET/CT scanners operate at low capacity due to a lack of reliable radiopharmaceutical supply.

Technology: Provides exclusive access to the IONETIX ION-12SC cyclotron, an FDA-cleared, ultra-compact superconducting system that is 80% smaller than traditional cyclotrons and enables on-site, on-demand production of isotopes like F-18, N-13, and Ga-68.

Comprehensive Solution: The model includes infrastructure development (site planning, shielding, installation), human capital development (training, certification), operational excellence (GMP-compliant radiopharmacy, workflow optimization), and clinical research integration (fast-track regulatory approvals, connections to sponsors).

Proven Success: The model's flagship partnership is with the Hospital Internacional de Colombia (HIC), the first South American member of the Mayo Clinic Care Network. The implementation resulted in a 3x increase in PET scan volume and established HIC as a regional center of excellence participating in theranostics trials.

The Specialized Service Ecosystem

The complexity of RLT trials has created a pivotal dependency on a small, specialized ecosystem of clinical support partners. Sophisticated sponsors are increasingly acting as "general contractors," assembling a bespoke coalition of best-in-class specialists. This ecosystem includes:

Clinical Site & Patient Support Specialists: (e.g., RadNet, UPPI, SOFIE Biosciences)

Hub-and-Spoke Delivery Model

This model is emerging as a viable near-term solution to the site access crisis. It involves a central, fully-equipped "hub" that handles complex radiopharmaceutical logistics and supports multiple community-based "spoke" sites. The 2024 partnership between Jubilant Radiopharma and Simplified Imaging Solutions (SIS) is a prime example, offering a turnkey service that consolidates the radiopharmaceutical, equipment, technologists, and licensing into a single fee, enabling community practices to participate in RLT trials.

5. Industry Perspectives and Key Quotes

Direct commentary from industry professionals underscores the key challenges and opportunities in the RLT space.

On the Unmet Need for Specialized Trial Sites:

RLT Business Development Executive:"This really ties into the story I am telling beautifully, which is there just aren't enough capable sites of doing the true advanced imaging. It's a major challenge in the industry."

Oncidium Foundation Member:"There is an unmet clinical need to develop these products more efficiently. Large RLT sponsors are having time finding adequate trial sites."

RLT Clinical Development Professional:"You’ve clearly built something with real potential, ORT’s integrated model, clinical depth, and focus on radioligand therapy trials fill a clear and growing need in the space."

On the Strategic Opportunity:

Nuclear Medicine Company CEO:"This is truly a perfectly timed opportunity. Your team composition, experience, and partner interest are very impressive, and I think your approach of focusing on trial speed, dosimetry expertise, and independence from traditional institutional delays is going to be a key differentiator."

On the State of the Clinical Support Ecosystem:

ProGen Search's View (CROs):"The CRO landscape for radiopharmaceuticals is a clear example of a market struggling to keep pace with scientific innovation. The field is consolidating around a handful of trusted 'Specialist Leaders'... creating a capacity bottleneck."

ProGen Search's View (Dosimetry):"The 'Dosimetry Mandate' is no longer a future prediction; it is a present-day reality... dosimetry has shifted from an exploratory endpoint to a required component of the data package used to justify dose selection."

ProGen Search's View (Talent):"We estimate that the demand for VPs of Clinical Development and CMOs with direct alpha-emitter experience now exceeds the available talent pool by a factor of 5 to 1."